Angola: Angola Energy Profile

2015/01/29

Background

Angola is the second-major oil producer in Sub-Saharan Africa behind Nigeria, and recent exploration suggests that Angola's reserves may be larger than initially estimated.

Angola's rapid rise as an energy producer over the completed two decades came despite a civil war that lasted until 2002 and without a lot of of the advantages found in other energy-rich regions. In particular, Angola lacked the appropriate infrastructure and the regulatory oversight necessary to operate a modern energy sector. With the end of the Angolan civil war in 2002, and steady investment in the country\\\'s energy infrastructure, the next of Angolan production is bright. Challenges remain—notably the tensions in the Cabinda province—but as the request for oil continues to rebound from the world recession, Angolan crude will be an significant resource for China, the United States, and other major energy importers.

Since becoming a member of the Organization of the Petroleum Exporting Nations (OPEC) in 2007, Angola's production levels have been subject to oversight by the group. However, Angola has not always acceded to the group\\\'s demands, and Angola's leadership plans to continue boosting production of oil and natural gas over the coming decade to help increase government revenue. In particular, Angola's offshore pre-salt formations and the construction of natural gas-processing facilities are viewed as potentially lucrative sources of next revenues.

Angola's economy is almost entirely dependent on oil production, as oil exports accounted for approximately 98 % of government revenues in 2011 according to the International Monetary Fund. High international oil prices will be significant for the next prospects of exploration, production, and exports of oil and natural gas, and will due affect Angola's government spending. In recent years, roughly three-quarters of Angola's total government revenues came from the energy sector.

With a gross domestic product (GDP) of over $104 billion in 2011 on the strength of its oil exports, Angola has the third-major economy in Africa. The International Monetary Fund estimates Angola's GDP per capita in 2011 was approximately $5,900 in current international dollars; however, much of the oil wealth in the country does not find its way to the average citizen, which is one of the reasons why nearly 60 % of primary energy consumption consists of solid biomass.

The August 2012 presidential election again brought the country's energy sector into the public discourse, as the management of profits from the export of crude oil became an issue of some importance. Over the completed decade, Angola made evolution towards better capturing and distributing the profits associated with its hydrocarbon industries—notably through its Oil Investment Fund—but opposition voices discord on the level of success the country has made. A policy of \\\"Angolanization\\\" intends to help the Angolan populace become additional integrated into the country's energy sector, and to obtain a better share of the wealth being generated by the country's oil exports. Additionally, in October of 2012 plans for a $5 billion sovereign wealth fund were announced. While such programs have not from presently on completed great success, Angolans remain optimistic that the government's efforts will succeed.

Oil

Successful exploration in Angola's pre-salt formations continues to drive optimistic oil production forecasts for the country, and the Angolan government is targeting 2 million barrel per day production levels by 2014.

According to Oil & Gas Journal estimates for the end of 2011, Angola had proved reserves of 9.5 billion barrels of crude oil. That figure is the second-major in Sub-Saharan Africa behind Nigeria, and ranks 18th in the world. Angola's crude oil is light and sweet, making it ideal for export to major world markets like China and the United States. Exploration and production in offshore Angola is advancing at a rapid pace, and foreign investors are beginning to consider some onshore opportunities economically viable. Exports continue to drive Angolan oil production, but the development of new refining capacity could help relieve domestic request shortages that have plagued the country since the end of the civil war in 2002. Prospects for increase in the oil sector are good, but instability and the threat of conflict continue to temper expectations.

Sector organization

In 1976, the government of Angola created a national oil company, the Sociedade Nacional de Combustiveis de Angola (Sonangol). In 1978, Sonangol became the sole concessionaire and majority shareholder in all oil and gas exploration in Angola, and took charge of all petroleum industry activities. Sonangol operates 17 subsidiaries throughout the oil and natural gas (and related) industries. Key subsidiaries include: Sonangol Pesquisa e Produção (P&P), which undertakes all exploration and production activities for Sonangol in Angola; Sonaref, which runs refining operations in Angola; and Sonagás, which is in charge of the exploration, production, and transportation of natural gas in Angola.

Foreign companies involved in Angola operate under joint venture operations and production-sharing agreements (PSAs) with Sonangol, and major partners include Chevron, ExxonMobil, British Petroleum (BP), Statoil, Eni, and Total, part others. China's Sinopec and the China National Offshore Oil Corporation (CNOOC) are as well involved in Angola, and are providing development assistance inclunding oil-backed loans and trade. Sonangol funds its operations though oil-backed borrowing, so finding partners able to provide such services is an significant goal for the company.

Sonangol is becoming additional involved in international ventures, and the company currently has interests in Brazil, Cuba, Iraq, São Tome and Principe, Venezuela, and in the Gulf of Mexico. Early in 2012, Sonangol pulled out of a natural gas project in Iran next a tightening of US-led sanctions on that country. Nevertheless, Sonangol continues to explore opportunities across the globe as it tries to establish itself as a major international player.

Over the completed few years, Angola instituted local-content (notably labor) requirements in its energy sector, but the so-called "Angolanization" regulations have from presently on to make a sizeable impact. The regulations require international companies operating in the country to meet a 70 % Angolanization threshold, but to date this figure has rarely—if ever—been met. Despite these requirements, less than 1 % of Angolans are employed in the energy sector, although the government hopes that will change as the technical capacity of its citizen's increases in the coming years. This may occur through the contributions to training programs that is presently required of all international oil companies doing business in Angola. Companies are expected to provide $200,000 per year, per block during the exploration phase of their operations to fund technical training programs, and $0.15 per barrel of oil during the production phase. These regulations are designed to improve the technical and financial capacity of Sonangol, its subsidiaries, and Angola's citizens. In 2011, Angola as well passed a law that requires the international oil companies to utilize the services of local banks.

Exploration and production

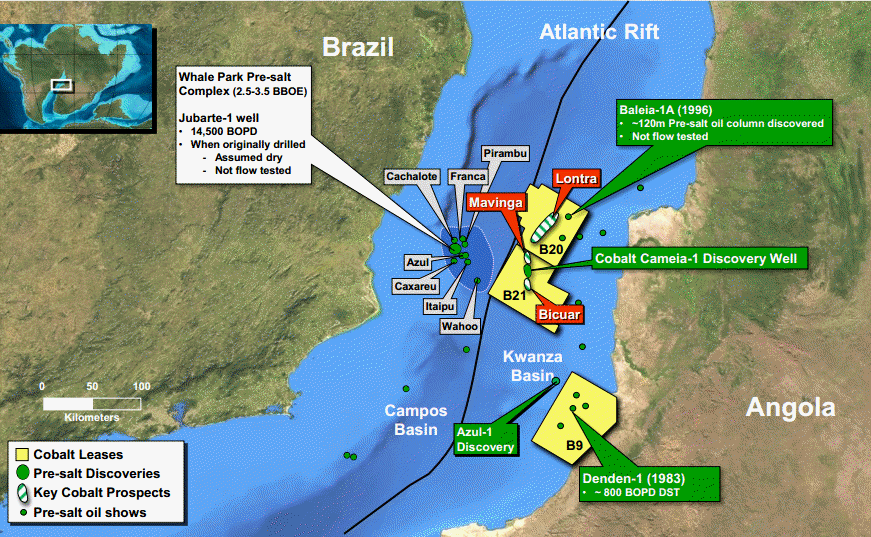

Exploration in Angola's offshore blocks continues to be successful, and recent forays into onshore blocks have been met with positive results. Angola's position as the second-major producer of crude oil in Sub-Saharan Africa, and as a member of the OPEC, means that international oil companies are by presently very familiar with the country4s resource endowments. Nevertheless, recent drilling success in Angola's pre-salt formations created a palpable buzz in the industry.

With Angola's crude being sweet (low in sulfur) and light, it is well-suited for exports to the United States, China, and other large importers, and the possibility of significant hydrocarbon resources in pre-salt formations has potential investors intrigued. This is due to the geological similarities between Angola's pre-salt formations and those of Brazil, which have remained largely unchanged since present-day South America and Africa split 165 million years ago. Because of the similar geology on the east coast of Brazil and the west coast of Angola (and its neighbors), a lot of petroleum geologists believe that the hydrocarbon formations of the two areas will be similar.

Angola's rise as a major oil-producing country came relatively recently due to the country\\\'s long civil war (1975-2002), which restricted exploration in the country. Once Angola began to stabilize its oil production increased dramatically, additional than doubling from 896,000 barrels per day (bbl/d) in 2002 to 1.84 million bbl/d of total liquids in 2011. Angola briefly challenged Nigeria as the top oil producer in Sub-Saharan Africa in 2009, but Angola\\\'s total liquid production declined slightly in 2010 and again in 2011. Crude oil production in Angola slipped to 1.79 million bbl/d in 2011, but the additions from new projects like the Kizomba Satellites should help Angola reverse that trend. These declines came as a result of regular maintenance and normal decline in the country's older fields, and Angola's government is targeting a return to the 2 million bbl/d production-levels it completed in 2008 by 2014.

Results of 2011 exploration and production licensing

| Block | Operator | Stake (%) |

|---|---|---|

| 19 | BP | 50% |

| 20 | Cobalt | 40% |

| 22 | Repsol | 30% |

| 24 | BP | 50% |

| 25 | Total | 35% |

| 35 | ENI | 30% |

| 36 | ConocoPhillips | 30% |

| 37 | ConocoPhillips | 30% |

| 38 | Statoil | 40% |

| 39 | Statoil | 40% |

| 40 | Total | 35% |

| Source: PFC Energy, company reports |

Refining and downstream

Angola has only one refinery, which was constructed in 1955 and has a capacity of just 39,000 bbl/d. On the horizon, however, is the new Sonaref refinery in Lobito, which is scheduled to begin operations in 2016. The refinery is expected to produce approximately 120,000 bbl/d initially, and will from presently on reach a 200,000 bbl/d capacity. It will be able to process heavy and acidic crudes, drawn from fields like Dalia and others like it. The project was originally to be built in partnership with China's Sinopec, but the Chinese company withdrew citing concerns about the current market for refined products. Sonangol is exploring possible collaboration with a number of other international oil companies, but to date no agreements have been reached. While the new refinery will help to meet domestic request for refined products, Angola will most likely remain heavily dependent on imports for the foreseeable next.

Consumption of refined products in Angola remains relatively low due to low levels of economic development across large segments of the people, but it is increasing steadily. In 2011, total consumption of oil products was approximately 88,000 bbl/d, up substantially from 75,300 bbl/d in 2009. Transportation fuel prices are part the lowest in the world due to national subsidies that have been in place for years; subsidies which equaled 7.8 % of GDP in 2011 (the equivalent of 90 % of the government's public investment spending).

Exports

The majority of Angolan crude oil is medium- to light-crude (30 degrees - 40 degrees API) and has low sulfur content (0.12 % - 0.14 %), making it ideal for export. With domestic consumption of under 100,000 bbl/d, nearly all of Angola's oil production is available for export. In 2011, Angola exported approximately 1.53 million bbl/d, with the major shares going to China (38 %) and the United States (14 %). In 2011, Angola was the second-major supplier of oil to China (behind only Saudi Arabia) and the 10th major supplier to the United States. All told, Angola exports nearly 80 % of its total oil production.

Angola has several export terminals, inclunding a lot of very large floating production, storage, and offloading (FPSO) vessels like the Sanha LPG FPSO and the Kizomba A FPSO. The Sanha vessel was the initial to combine all the LPG processing and export functions on the same vessel; it is as well the major of its kind. The Kizomba A has a storage capacity of 2.2 million barrels of oil, and is one of the major vessels of its kind in the world (perhaps even the major).

Natural gas

With the initial cargo of liquefied natural gas (LNG) scheduled to leave Angola in early 2013, the country is in a position to capitalize on the high request for LNG to bolster its export portfolio.

According to Oil and Gas Journal estimates, at the end of 2011 Angola had proved reserves of natural gas of 10.95 trillion cubic feet (Tcf). That is the fifth-major endowment in Africa, and ranks second in Sub-Saharan Africa behind only Nigeria. While the majority of Angolan natural gas is re-injected into the countr\'s oilfields to aid recovery—or simply flared off—efforts are underway to enhance Angola's ability to produce and market its natural gas reserves. To date, these efforts have been focused on the development of the country's initial liquefied natural gas (LNG) terminal at Soyo. With operations set to begin in early 2013, Angola should be able to capitalize on the recent request spike for LNG cargoes resulting from Japan's continued shuttering of its nuclear program.

Angola's natural gas sector is run through a subsidiary of national oil company Sonangol, called Sonangás. Sonangás was formed in 2004, and is tasked with the exploration, evaluation, production, storage, and transport of Angola's natural gas and natural gas derivatives. Sonangás is working with Sonangol P&P to establish a regulatory environment—inclunding taxation—to help spur research and development in the natural gas sector of Angola.

Exploration and production

Natural gas production in Angola has additional than tripled over the completed two decades, growing from 98 billion cubic feet (Bcf) in 1990 to 379 Bcf in 2011. The vast majority of Angolan natural gas is re-injected into oil fields to help recovery, or it is simply flared off as a by-product of oil operations. In 2011, re-injection and flaring accounted for 91 % of all the natural gas produced in the country. Angola's natural gas production comes almost entirely from associated fields, but the completion of the Soyo LNG facility (Angola LNG) could begin raising the incentives for natural gas production in the country.

Chevron's $1.9 billion Sanha project (located offshore near Soyo) began operations in 2005, and is able to process 100,000 bbl/d of oil, condensate, and liquefied petroleum gas (LPG). The project significantly reduced the need for gas-flaring in Areas A, B, and C in Block 0 (shown on map), as the roughly 500 million cubic feet per day (MMcf/d) of dry gas (which is what remains next the raw product is stripped of condensate and LPG) will be re-injected into the Sanha reservoir to help with oil recovery operations. This process is estimated to both reduce flaring in Block 0 by at least 50 % and to reduce carbon dioxide emissions by additional than 2 million tons per year according to Offshore magazine.

With offshore oil exploration continuing apace, Angola will need to address its capacity for processing the large volumes of associated gas its oil operations will inevitably produce. Enhancing LNG capabilities, developing the domestic market for natural gas—specifically commercial customers—and enhanced oil recovery techniques will all be significant components of Angola's natural gas strategy moving forward.

Liquefied natural gas

Central to Angola's plan of reducing flaring and monetizing its significant natural gas reserves is the LNG facility at Soyo, which was completed in 2012. The Angola LNG project is a joint venture between Sonangol (22.8 %), Chevron (36.4 %), Total (13.6 %), BP (13.6 %), and Eni (13.6 %), and is slated to process 1 billion cubic feet (Bcf) per day of natural gas for domestic and international markets. The facility has a capacity of 5.2 million tons per year of LNG, and will as well provide up to 125,000 cubic feet per day of natural gas for domestic consumption. Plans call for the gas to be sourced from Blocks 0, 1, 2, 14, 15, 17 and 18.

According to Angola LNG—the Sonangol subsidiary in charge of the project in Soyo—the project represents the major single investment in Angola in history. Operations were set to begin in the initial quarter of 2012, but numerous delays pushed the scheduled start date back to the beginning of 2013. Angola LNG has seven LNG carriers at its disposal, each with a capacity of 160,000 cubic meters, though due to the delays at the facility in Soyo several of the vessels have been contracted out to other companies. Initial plans called for the LNG cargoes to be shipped to a re-gasification facility in Pascagoula, Mississippi operated by Gulf LNG; however, the market conditions in the United States are no longer favorable due to the gas-glut caused by the boom in unconventional gas. Instead, Angola LNG is targeting consumers in Europe and Asia, and is rumored to want to send its initial shipment to fellow Lusophone country Brazil.

Electricity

Angola's fractured electricity system serves 30 percent of the population and progress towards providing greater access is proving difficult. The Angolan government plans to invest billions of dollars in the country's electricity system, but in the short-term access to power will remain a challenge.

Angola's electricity sector is run almost exclusively by the state company Empresa Nacional de Electricidade (ENE), but some private companies in the extractive industries have built power plants to run their operations. Angola is a member of the Southern African Power Pool (SAPP), a group that includes Botswana, the DRC, Lesotho, Malawi, Mozambique, Namibia, South Africa, Swaziland, Tanzania, Zambia, and Zimbabwe. The SAPP is designed to promote cooperation between member countries with the aim of creating a common electricity market that can provide reliable, and affordable, electricity to the citizens of member countries.

At present, Angola does not have a national electricity grid, instead relying on three independent systems that provide electricity to different parts of the country: The Northern, Central, and Southern Systems. The Northern System is connected to the Cuanza river basin and is the country's largest, serving the country's capital, Luanda. The Central and Southern Systems are linked to the Catumbela and Cunene river basins, respectively. The government hopes to link the three independent grids as part of a national grid system, and eventually to link its grid with neighboring SAPP members.

Currently, only 30 percent of Angolans have regular access to electricity, with that figure declining to below 10 percent in rural areas according to IHS. Limited existing infrastructure and a lack of funding for the power sector mean that Angola's ability to improve these rates substantially is limited. In late 2011, the Angolan government announced that it intends to invest $16 billion in the electricity sector by 2016 in an effort to improve the country's transmission and distribution networks, and to help bring electricity to the country's remote rural regions. The plan proposes to increase overall electricity supplies by 12 percent in order to help meet rising domestic demand.

In 2010, over 68 percent of Angola's electricity was generated at the country's hydroelectric facilities, primarily from hydroelectric dams on the Cuanza, Catumbela, and Cunene rivers. Some analysis suggests that the country's potential hydroelectric generating capacity is well over 10 times the currently-installed generating capacity, but tangible plans to develop the country's hydroelectric resources have not yet emerged. The largest facility is the Capanda hydropower dam, which has installed capacity of 520 megawatts.

Given Angola's vast natural gas reserves, thermal generation is likely to gain increasing importance in the coming years. There have been discussions about building gas-fired facilities near the country's oil operations, in part to support industry there, but firm proposals have yet to emerge. In that same vein, in 2006 Angola began discussions with the International Atomic Energy Agency about developing a domestic nuclear power program, but details remain scarce and any project is still decades away from becoming a reality.

- Angola News

-

- ANGOLA: Angola's Elections Trigger a Crisis of Legitimacy

- ANGOLA: Congo's Sassou hails retiring dos Santos for service to Africa

- ANGOLA: Angolan opposition parties formally challenge election results in court

- ANGOLA: Submarine cable deployed in Angola to link Africa to South America

- AFGHANISTAN: UNWTO: International tourism – strongest half-year results since 2010

- BOTSWANA: Why governments need to support the financial sector to meet the unserved needs of smallholder farmers

- Trending Articles

-

- SOUTH AFRICA: Nigeria and South Africa emerge from recession

- BAHRAIN: Bahrain issues new rules to encourage fintech growth

- UZBEKISTAN: Former deputy PM named Uzbekistan Airways head

- ARUBA: Director of Tourism Turks and Caicos after Irma: Tourism, visitors, hotels current status

- ANGOLA: Angola: Elections / 2017 - Provisional Data Point Out Qualified Majority for MPLA

- WORLD: How fair is our food? Big companies take reins on sourcing schemes

.gif?1356023993 "Business Park of Mauritius Ltd, Mauritius")